Debt Crisis Shift to The Emerging Market Countries

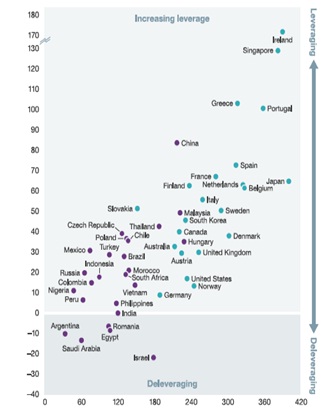

The post-crisis success of emerging market countries (such as: China, Brazil, Russia, India and Indonesia) demonstrated that they had become significantly more resilient in the years prior to the crisis. Yet it certainly does not imply they have decoupled from what happens in developed countries. The credit boom in emerging market economies was in large part a response to the credit bust in developed countries, mainly in the United States. Obstfeld (as cited in The Economist, 2015) finds that credit booms have been one of the two best predictors of crisis in emerging markets, the other is a rapidly appreciating of real exchange rate. As the consequences of the credit bubbles in the United States turned to bust, sending interest rates to historic lows, and shifted the direction of capital flow. Financial capital flows from the developed or high income countries to financing projects or purchasing assets in emerging market countries. According to the figure 1, overall debt in emerging markets, for instance, in China has jumped to 195 % of Gross Domestic Product (GDP) in 2014.

The post-crisis success of emerging market countries (such as: China, Brazil, Russia, India and Indonesia) demonstrated that they had become significantly more resilient in the years prior to the crisis. Yet it certainly does not imply they have decoupled from what happens in developed countries. The credit boom in emerging market economies was in large part a response to the credit bust in developed countries, mainly in the United States. Obstfeld (as cited in The Economist, 2015) finds that credit booms have been one of the two best predictors of crisis in emerging markets, the other is a rapidly appreciating of real exchange rate. As the consequences of the credit bubbles in the United States turned to bust, sending interest rates to historic lows, and shifted the direction of capital flow. Financial capital flows from the developed or high income countries to financing projects or purchasing assets in emerging market countries. According to the figure 1, overall debt in emerging markets, for instance, in China has jumped to 195 % of Gross Domestic Product (GDP) in 2014.

In China total debt has quadrupled, going up from $7 trillion in 2007 to $28 trillion in midyear 2014 fueled by real estate and shadow banking activity (McKinsey, 2015). There is growing concern if the potential increase of the US Federal Reserve rate this December 2015 could reduce capital flows to emerging markets, which potentially raising borrowing costs even if central banks do not raise policy rates in order to support their currencies. Given the scale of debt in the most highly indebted countries, the current solutions for sparking growth or cutting fiscal deficits alone will not be sufficient. New approaches are required to start deleveraging and to supervise and monitor debt. High debt levels, whether in the public or private sector, have historically placed a drag on growth and raised the risk of financial crises that spark deep economic recessions.